When people think about risk in investing, they often focus on market crashes.

But the real danger that quietly eats away at your wealth is inflation.

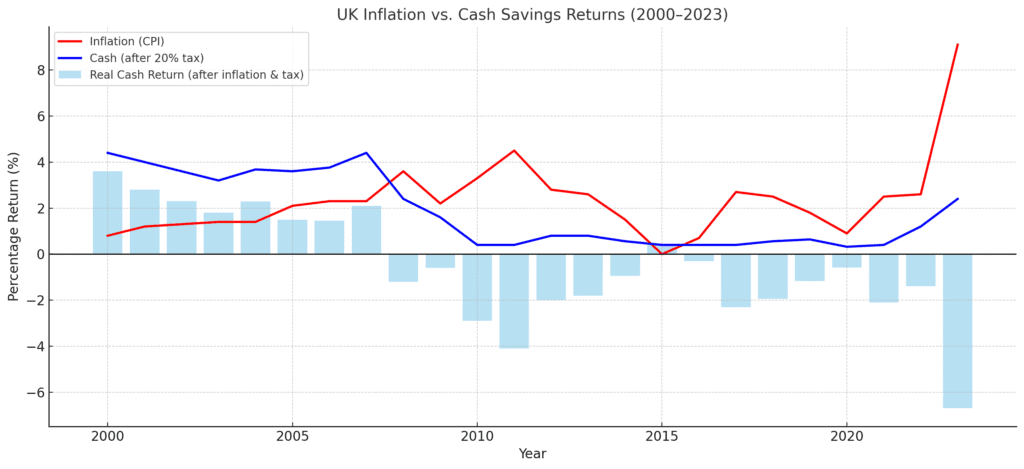

Over time, rising prices reduce the real value of your money. That’s why you need to look at real returns — the return you get after inflation and tax.

Cash and the Problem of Negative Real Returns

On paper, cash feels safe. You can see it in your account and it doesn’t fluctuate in value. But history shows that cash rarely keeps pace with inflation, especially once you deduct tax on interest.

- If inflation is 4% and your savings account pays 3%, you’re already losing 1% in purchasing power.

- Add in 20% tax on the interest, and your real loss is even bigger.

- Over decades, this can be devastating — £100 left in cash for 20 years in a 3% inflation world is only worth around £55 in today’s money.

The lesson: cash is useful for short-term needs and emergencies, but a poor store of long-term wealth.

Why Real Assets Offer Better Protection

“Real assets” are investments tied to tangible things: property, infrastructure, farmland, commodities. Their value often moves with inflation because they’re linked to the real economy.

- Property & infrastructure: Rents and usage fees can be adjusted upwards over time.

- Equities: Companies producing real goods and services can increase prices to offset rising costs.

- Commodities: Oil, copper, wheat, gold — their prices often rise directly in response to inflation.

By holding some of these, investors get natural protection that cash simply doesn’t provide.

Companies That Can Pass on Price Increases

Not all companies handle inflation equally. The best positioned are those with:

- Pricing power – Strong brands or market positions that allow them to raise prices without losing customers (think Apple, Unilever, Nestlé).

- Essential products – Goods people buy regardless of price, like consumer staples, healthcare, or utilities.

- Flexible cost bases – Firms that can adjust quickly to higher input costs.

These businesses can maintain profit margins even when inflation is high, making their shares more resilient.

Commodities as an Inflation Hedge

Periods of high and rising inflation — like the 1970s or more recently in 2021–2022 — often see commodities outperform.

- Energy: Oil and gas prices tend to surge with inflation, especially when supply is constrained.

- Precious metals: Gold has historically been viewed as a store of value in times of currency debasement.

- Broad baskets: Commodity indices track agricultural and industrial inputs that benefit from higher demand and rising prices.

Holding commodities isn’t a long-term growth strategy, but they can be a useful diversifier during inflationary spikes.

Key Takeaways

- Inflation quietly erodes the real value of cash, especially after tax.

- Real assets like property, infrastructure, and equities can help preserve purchasing power.

- Companies with pricing power fare best in an inflationary environment.

- Commodities can provide a hedge when inflation is high and rising.

✅ Action Point for Readers: Look at your portfolio and ask: how much of it is vulnerable to inflation? In times of higher inflation, consider balancing cash holdings with real assets and exposure to businesses or commodities that can withstand rising prices.