If you’ve ever looked at investing and thought, “I don’t have the time to pick individual shares,” that’s exactly what ETFs were designed to solve.

An ETF (Exchange-Traded Fund) is a ready-made basket of investments—packaged into a single fund you can buy and sell on the stock market, just like a share.

That simple idea brings some big benefits.

What an ETF actually is (in plain English)

Most ETFs are built to track an index.

An index is just a rule-based list of investments. For example:

- The FTSE 100 is (roughly) the 100 largest companies listed in the UK.

- The S&P 500 is 500 large US companies.

- A global index might hold thousands of companies across many countries.

An ETF that tracks the S&P 500 aims to deliver returns that closely match the S&P 500 (minus a small fee). It does this by holding the underlying shares (or using other methods—more on that later).

Because ETFs trade on an exchange, you can generally buy or sell them during market hours, in real time.

Why investors use ETFs: the key benefits

1) Instant diversification

Diversification means “don’t put all your eggs in one basket.”

- Buy one global equity ETF and you may own hundreds of companies.

- Buy one bond ETF and you can spread risk across many issuers and maturities.

This reduces the damage any single company (or bond issuer) can do to your portfolio.

2) Low cost

Most “plain vanilla” index ETFs are cheap to run because they follow rules rather than paying managers to pick stocks. The ongoing fee is shown as the OCF (Ongoing Charges Figure).

Small differences in fees compound over time, so cost matters.

3) Simplicity and flexibility

ETFs make it easy to build a portfolio with a few building blocks:

- Global shares

- Global bonds (or UK gilts)

- Inflation-linked bonds

- Cash-like short-term bonds

- Property (REITs) or smaller “satellite” themes if you want them

4) Transparency

Most ETFs publish their holdings and clearly state:

- The index they track

- The fees

- The fund size

- The currency and dealing details

5) Tax wrappers and accessibility (UK)

ETFs are widely available on UK platforms and can be held in:

- Stocks & Shares ISA

- SIPP

- General investment account (taxable)

That flexibility makes them a natural fit for DIY investors.

The different types of ETF indices you can buy

Here are the most common “index families” you’ll see when choosing ETFs:

A) Equity (shares) indices

- UK: FTSE 100, FTSE 250, FTSE All-Share

- US: S&P 500, Russell 1000/2000, Total Market

- Global developed: MSCI World / FTSE Developed World

- All-country global: MSCI ACWI / FTSE All-World (developed + emerging)

- Emerging markets: MSCI Emerging Markets / FTSE Emerging

Practical tip: many UK DIY investors start with a global all-world equity ETF as a core holding.

B) Bond indices

Bond ETFs are often grouped by:

- Issuer: government bonds (gilts/treasuries) vs corporate bonds

- Credit quality: investment grade vs high yield

- Maturity: short / intermediate / long duration

- Inflation-linked: linkers (UK index-linked gilts) or global inflation-linked bonds

Bond indices matter because bond behaviour changes a lot with maturity and credit risk.

C) “Factor” indices (rule-based tilts)

These follow rules like:

- Value (cheaper shares)

- Quality (profitable, stable businesses)

- Small-cap

- Momentum

- Low volatility

They can be useful, but they behave differently from the broad market and can underperform for long stretches.

D) Sector / thematic indices

Tech, healthcare, clean energy, robotics, AI, etc.

These can be exciting but often:

- are more concentrated

- cost more

- are “story-driven”

- can be volatile

For most people, they’re best kept as a small “satellite” allocation (if at all).

E) Commodity and alternative indices

Gold ETFs are common; broad commodity ETFs exist too (often using futures).

These can diversify, but they come with their own mechanics and risks.

The risks to understand (and how they show up)

1) Market risk

If the market (shares or bonds) falls, your ETF falls too.

An ETF doesn’t remove risk—it spreads it. You’re still exposed to the ups and downs of the underlying markets.

2) Currency risk (a big one for UK investors)

If you buy a US or global ETF, the underlying assets are priced in foreign currencies.

That means your returns in pounds depend on:

- the market return and

- what GBP does versus USD/EUR/JPY, etc.

Sometimes currency helps you, sometimes it hurts you. Over short periods it can impact returns.

Hedged vs unhedged:

Some ETFs offer a GBP-hedged version (designed to reduce currency swings). Hedging can reduce volatility, but it costs money and isn’t perfect. Many long-term investors keep global equities unhedged and may consider hedging for parts of their bond allocation (where currency can overwhelm the bond yield).

3) Provider risk (and fund structure risk)

If an ETF provider (the company behind it) got into trouble, your assets are typically held in a ring-fenced fund structure—not sitting on the provider’s balance sheet.

But there are still risks worth checking:

- Fund domicile and structure (e.g., UCITS for UK/Europe investors is common)

- How the ETF tracks the index (physical vs synthetic)

- Securities lending (some funds lend shares to earn extra income; read the policy)

- Counterparty risk (more relevant to synthetic ETFs)

In practice, major providers and large UCITS ETFs are widely used, but it’s still sensible to understand the structure. You may just wish to stick with the larger providers.

4) Tracking risk (tracking difference)

Even index ETFs won’t match the index perfectly because of:

- fees

- trading costs

- taxes within the fund (varies by market and structure)

- how dividends are handled

This is why it’s useful to look at historical tracking difference, not just the OCF (charges).

5) Liquidity and trading costs

Most big ETFs are very liquid (i.e. you can easily buy and sell these), but your cost to get in/out can include:

- dealing fee (platform)

- bid–offer spread (difference between buy and sell price)

For very niche or tiny ETFs, spreads can be wider.

How to choose an ETF: a simple checklist

Step 1: Decide the job the ETF must do

Ask: What role is this holding meant to play?

- Core global equity exposure?

- UK tilt?

- Defensive bonds?

- Inflation protection?

- Small satellite theme?

Start with the role, not the product list.

Step 2: Choose the right index

Two “global” indices can be meaningfully different:

- Does it include emerging markets?

- Is it large-cap only or total market?

- How concentrated is it in the US?

- Does it exclude certain sectors (e.g., ESG screens)?

Step 3: Check the ETF structure

Look for:

- UCITS (common for UK investors)

- Physical replication (holds the underlying shares/bonds) vs synthetic (uses swaps)

- Accumulating vs distributing:

- Accumulating (Acc) reinvests income automatically

- Distributing (Dist/Inc) pays income out as cash

For many long-term investors in an ISA/SIPP, accumulating can be simpler.

Step 4: Compare costs properly

Check:

- OCF

- Typical bid–offer spread

- Any platform dealing/holding costs

- Tracking difference (if available)

Cheapest isn’t always best, but all else equal, cost matters.

Step 5: Check size, age, and liquidity

Prefer ETFs that are:

- reasonably large (more established)

- have good trading volume

- from a well-known provider

Step 6: Know what you’re really exposed to

Before buying, look at:

- Top holdings (concentration risk)

- Country exposure

- Sector exposure

- Currency exposure

This avoids surprises like “I bought global, why is it 70% US?”

Where to find reliable information

When researching an ETF, these are the most useful sources:

- The ETF provider’s factsheet / KID (Key Information Document)

Look for: objective, index tracked, fees, risks, holdings, and tracking approach. - Your investment platform’s ETF page

Useful for: dealing currency, trading hours, costs, and sometimes comparison tools. - Independent ETF screeners

JustETF (popular in Europe/UK) and similar screeners are useful for filtering by index, fees, domicile, distributing vs accumulating, and hedging options. - Index provider websites (MSCI, FTSE Russell, S&P Dow Jones Indices)

Best place to understand what an index actually includes and how it’s built.

A sensible “starter” way to use ETFs

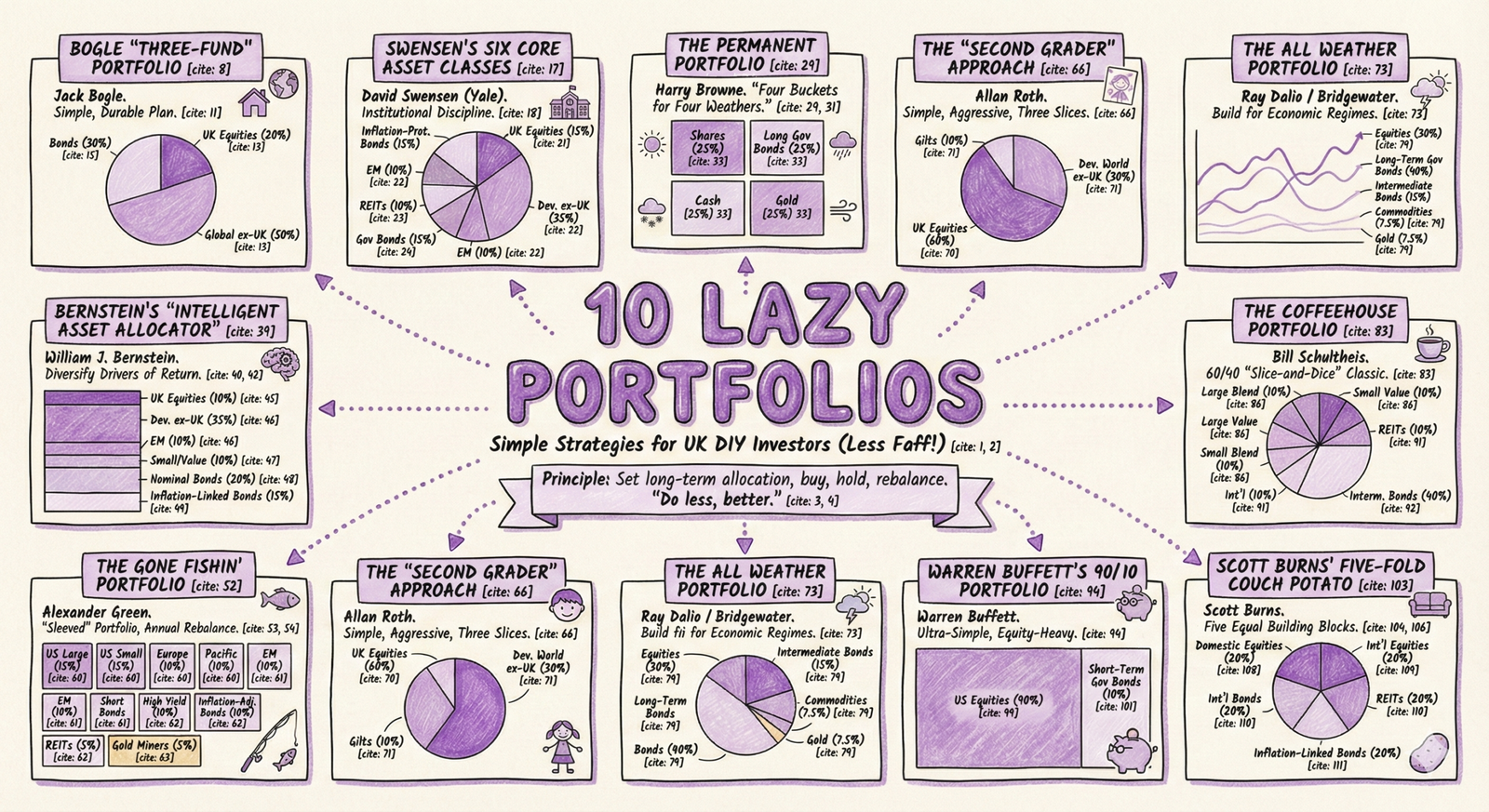

A common ETF-based approach is a core + optional satellites structure:

- Core: one global equity ETF + one bond ETF (or gilts) in a ratio that matches your risk tolerance

- Satellites (optional): small tilts (UK home bias, small-cap, value, property, gold, etc.)

It keeps things simple, diversified, and easy to rebalance.

Friendly reminder (important)

This is education, not personal financial advice. ETFs reduce complexity, but they don’t remove risk. The “best” ETF depends on your goals, time horizon, and how much volatility you can live with.

If you want, tell me what kind of investor the post is aimed at (e.g., “new to investing”, “building an ISA”, “near retirement”), and I’ll add a short “example ETF shortlist checklist” section tailored to that reader type—without naming specific products unless you want that.