This article is for educational purposes only and does not constitute personal financial advice. Please seek advice from a qualified financial adviser before making investment decisions.

A Common Question

“I don’t want to invest my money in the stock market — what do I do if I want a guaranteed income over the next few years?”

This is one of the most common questions from investors sitting on cash who are understandably cautious about equity markets. The good news is there is a compelling, time-tested strategy that uses the safety of UK government bonds to deliver predictable, tax-efficient income — a bond ladder.

This article explains how a bond ladder works for UK investors, the significant tax advantages for basic and higher rate taxpayers, and walks through a worked example of someone with £500,000 wanting to generate £30,000 per year.

How Should I Manage My Money?

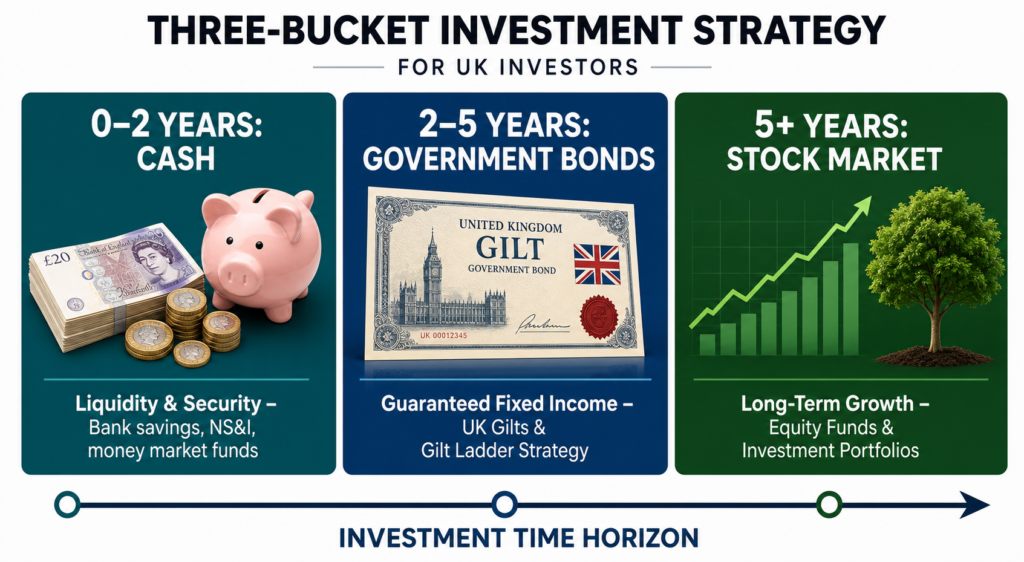

Before thinking about into bond ladders, it is worth thinking about different investments and your time horizons:

| Time Horizon | Asset Class | Purpose |

| Immediate (0–12 months) | Cash (savings account, NS&I) | Liquidity — accessible at any time |

| Short term (1–5 years) | UK Government Bonds (Gilts) | Predictable, fixed income with tax advantages |

| Long term (5+ years) | Equities / investment funds | Growth, inflation protection over time |

For someone who does not want stock market exposure in the short term, the middle column — UK government bonds — offers a good solution. You get a guaranteed return if you hold to maturity, backed by Government.

What Is a UK Government Bond?

A UK Government bond, or gilt, is an IOU issued by the UK Government.

When you buy a gilt, you are lending money to the Government. In return, you receive:

- A fixed coupon — an interest payment, usually twice a year.

- A fixed repayment at maturity — normally £100 for every £100 nominal of gilt held.

That second point matters.

Gilts trade in the market at prices above or below £100. If a gilt is priced at £90, you are paying about 90p for £1 of future repayment. If you hold it to maturity, you receive £1 back per £1 nominal, assuming the UK Government meets its obligations.

So the return comes from two places:

The capital uplift from the price you below the £100 maturity value.

The coupon income while you hold it.

The Return or Yield to Maturity (‘YTM’)

The Yield to Maturity (YTM) is the most important number for gilt investors. It represents the total annual return you will receive. This is the annualised return you should receive if:

- you buy the gilt at today’s price,

- you hold it until maturity,

- the UK Government repays as expected,

- and the coupons are received as scheduled.

In plain English:

Yield to maturity is the return that you can use to compare Government Bonds with the return from different investments.

The UK Debt Management Office uses gilt yield formulae based on the present value of future coupon payments and the final redemption payment. It also confirms that conventional gilts pay coupons in two semi-annual payments.

Example:

TN28 – ⅛% Treasury Gilt 2028

- Current price: £93.14

- Maturity date: 31 January 2028

- Coupon or interest payment: 0.125%

- Gross redemption yield: 4.31%

That means you are not getting much taxable interest. Most of the return comes from buying below £100 and receiving £100 at maturity. Currenct data currently shows a yield to maturity of 4.31% and a maturity date of 31 January 2028. These figures are correct at the time of writing this blog, and will change.

Why Now?

Currently there is a combination of:

- Persistent inflation forcing the Bank of England to maintain higher interest rates for longer

- Political uncertainty — both domestically and globally — pushing investors to demand higher returns for lending to governments

- Elevated government borrowing in the UK, increasing the supply of gilts and pushing yields higher

The UK 2-year gilt yield has been trading around 3.88–4.55% in recent months. For context, the 10-year yield was below 1% as recently as 2021. For income-seeking investors, this represents an opportunity not seen since before the 2008 financial crisis.

As gilt yields have risen, their prices have fallen — meaning you can now buy many gilts at a significant discount to their £100 maturity value, locking in that capital gain as a tax-free return.

The Tax Advantages of Low-Coupon Gilts

This is where gilts become particularly powerful for UK investors — and especially for higher rate taxpayers.

The tax treatment of gilts is straightforward:

- Coupon income is taxed as income at your marginal rate (20%, 40%, or 45%)

- Capital gains (the profit from buying below £100 and receiving £100 at maturity) are completely exempt from Capital Gains Tax (CGT)

This distinction is crucial. Low-coupon gilts — like those discussed in this article — are priced significantly below £100 because their coupons are tiny. Most of the return comes as a tax-free capital gain at maturity, not as taxable income.

Tax Comparison: Basic vs Higher Rate Taxpayer

Take a gilt with a current YTM or return of approximately 4.3%, a purchase price of around £93, and a maturity value of £100.

For a higher rate taxpayer, a cash savings account paying 4% gross yields just 2.4% after tax. The same gross return from a low-coupon gilt, where almost all the return is a tax-free capital gain, retains close to 3.9% net. That is a significant advantage that compounds over several years.

Example: A higher rate taxpayer earning 4.3% gross from a low-coupon gilt holds most of that return as a tax-free capital gain at maturity. A bank account at 4% is fully taxable as income — netting just 2.4% after 40% income tax.

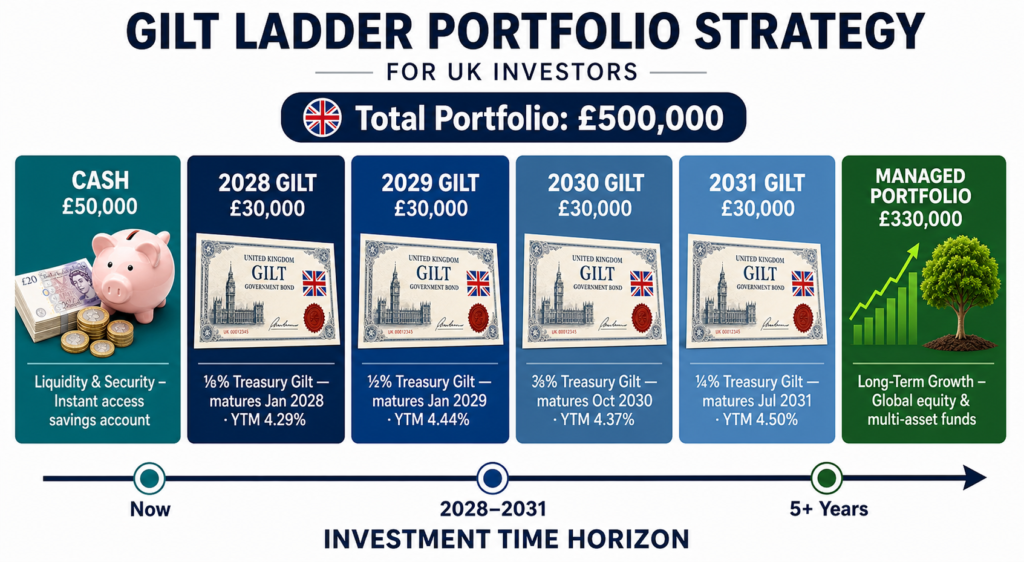

A Worked Example

Let’s say someone has £500,000 in cash and wants to take £30,000 a year for the next few years.

They do not want stock market risk for near-term spending. But they also do not want all £500,000 sitting in cash forever.

A simple structure could look like this:

Note: These YTM were correct as at 12th May 2026, there are links below to check current yields.

This is not perfect year-by-year matching because the gilt maturity dates do not all fall exactly 12 months apart. In practice, you would keep a cash buffer to smooth the timing.

But you can understand the idea:

The first year’s income is held in cash.

Future spending is matched to gilt maturities.

The rest can be invested for the longer term.

This is a worked example to illustrate the concept and is not personal financial advice. Actual prices, yields, and amounts invested will differ.

Benefits of This Strategy

- Guaranteed return: The UK government has never defaulted on a gilt. If you hold to maturity, you receive exactly £100 per bond, regardless of market conditions

- Fixed income: Once you purchase the bond, the YTM is locked in. There are no surprises from interest rate movements if you do not sell early

- Tax efficiency: Low-coupon gilts deliver most of their return as a tax-free capital gain, making them especially attractive for basic and higher rate taxpayers compared to cash savings

- Simplicity and transparency: You know exactly when your money is coming back and exactly how much you will receive

- No fund charges: Buying gilts directly means no annual management fees eating into your return

Risks to Be Aware Of

- Selling before maturity: If you need to sell a gilt before its maturity date, the price is determined by the market, which fluctuates with interest rates. The sale price will change as market conditions change.

- Inflation risk: While the return is fixed in nominal terms, inflation could erode the real purchasing power of your £30,000 annual income.

- UK government credit risk: Gilts are backed by HM Treasury. While the UK has an excellent credit history, a severe deterioration in public finances is an unlikely but theoretical risk.

Summary and Next Steps

A gilt bond ladder is a powerful, simple strategy for investors who want guaranteed, tax-efficient income over a defined period without relying on the stock market. With UK gilt yields near multi-decade highs, the opportunity to lock in 4–4.5% returns — largely tax-free for higher rate taxpayers — is as compelling as it has been in over fifteen years.

Practical next steps:

- Document your income requirements — how much do you need each year, and for how long?

- Understand your tax position — are you a basic, higher rate, or additional rate taxpayer? This determines how much benefit you get from the capital gains exemption

- Open a dealing account — platforms such as Hargreaves Lansdown, Interactive Investor, or AJ Bell allow you to buy and sell gilts directly. Some allow you to hold them within a Stocks & Shares ISA, where all returns are completely tax-free

- Look up current gilt prices and yields on the HM Treasury / DMO website at www.dmo.gov.uk or platforms such as dividenddata.co.uk or giltsyield.com

- Consider speaking to a financial adviser to ensure this strategy fits within your overall financial plan, tax position, and investment objectives

This article is for educational and informational purposes only. It does not constitute personal financial advice or a recommendation to buy or sell any investment. Investments can fall as well as rise in value, and you may not get back the full amount invested. Tax treatment depends on individual circumstances and may be subject to change. Always seek advice from a qualified, regulated financial adviser before making investment decisions.

© Clearly Investments