With the UK May elections later this week, it is worth considering any implications for your investment portfolio. Particularly what happens if the vote moves to one party or another. This article considers what history tells us, and what this may mean.

Need-to-knows

- When we think about the UK, it is important to remember, the FTSE 100 is not the UK economy. Over 75% of FTSE 100 revenue comes from overseas, so many of its biggest companies are driven more by global events than what happens here.

- The FTSE 250 is much more UK-sensitive. Almost half the revenue generated by companies in this index comes from the UK. This markey is more sensitive to UK events.

- Politics often hits sterling and government bonds more. That is where markets price in worries about deficits, credibility and future interest rates.

- Elections matter, but policy shocks matter more. The clearest example is the September 2022 mini-budget, which impacted the pound and government bond yields.

- For long-term investors, the real question is not who is in power. It is whether the policies makes the Government look stable, investable and credible.

History: do markets do better under Labour or Conservative governments?

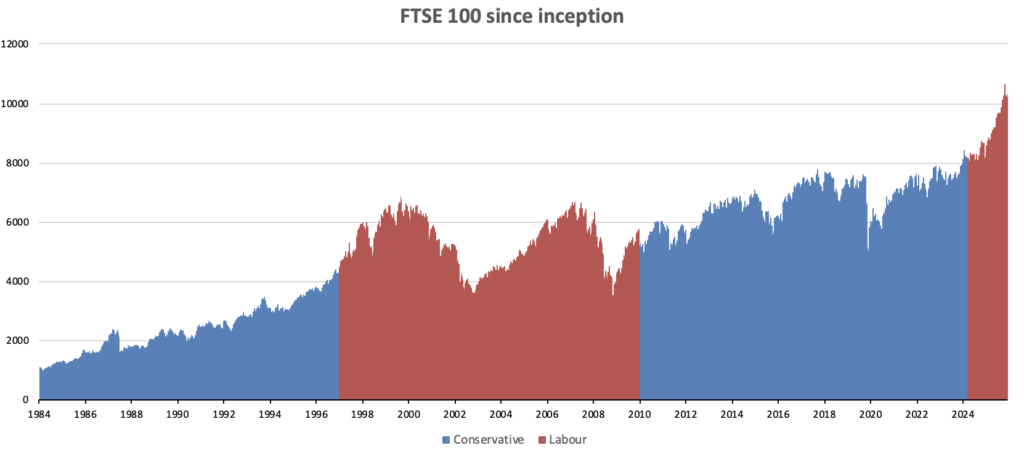

The FTSE 100 has broadly risen under governments of both colours since its launch in 1984. What matters far more than the party in power is what they inherited, the state of the global economy, interest rates, and commodity prices. The Conservatives were in power during Black Wednesday in 1992, the dot-com crash in 2000 was under Labour, the 2008 financial crisis (again Labour), and the COVID crash in 2020. None of those market shocks were caused by domestic politics, but global events.

So the historical lesson is simple: party control matters, but starting valuations, global crises, inflation, rates, commodity prices and confidence usually matter more.

How markets react to UK politics

FTSE 100: not a reflection of the UK Economy

The FTSE 100 sounds like UK economy. It is not. Around three quarters of FTSE 100 revenues come from overseas. The index is heavily influenced by things like oil prices, US growth, China demand, mining prices and currency moves.

That is why bad UK news does not always affect the FTSE 100. In fact, a weaker pound can sometimes help the index, because overseas earnings are worth more when translated back into sterling. It is one reason the blue-chip index can look oddly calm when the domestic mood is awful.

FTSE 250: where politics has a bigger impct

The FTSE 250 is the better place to look if you want to see how markets feel about UK politics. It is a more domestically focused index.

Here you get exposure to:-

- UK growth expectations

- consumer confidence

- housebuilding

- interest rates

- domestic regulation

You saw that clearly after Labour’s 2024 election win. The FTSE 250 jumped as much as 1.8%, homebuilders and construction shares surged, sterling firmed and 10-year gilt yields dipped. Markets liked the removal of political chaos and the prospect of greater stability.

So when people ask, “How do markets react to UK politics?”, the best answer is:

The FTSE 100 often reacts less than you expect. The FTSE 250 often reacts more than you expect.

The real impacts: sterling, gilt yields and interest-rate expectations

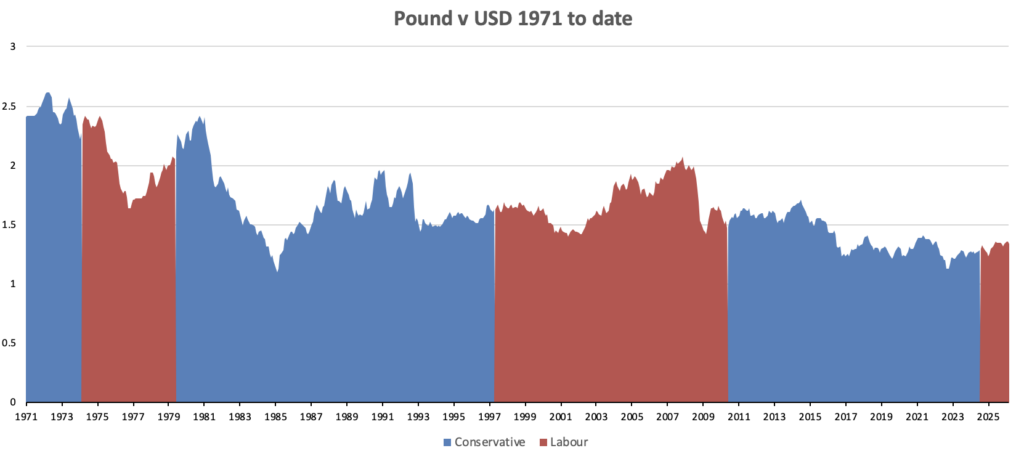

1) Sterling

The pound is often the fastest scoreboard for political confidence.

When investors think UK policy is sensible and stable, sterling can strengthen. When they fear policy chaos, weak growth or fiscal slippage, it can fall. During the mini-budget crisis, sterling plunged to a record low of $1.0327 in thin Asian trading. In April 2026, by contrast, the pound jumped to about $1.342 after the US-Iran ceasefire lifted global risk appetite and oil prices fell.

A falling pound matters because it can make imports more expensive, worsen inflation pressure and squeeze consumers. A stronger pound can ease some of that pressure, though it may reduce the translation boost for overseas earners in the FTSE 100.

2) Gilt yields

Gilts are where markets judge whether they trust the government’s sums.

If investors worry that borrowing is rising too fast, that tax plans do not add up, or that a government may abandon its own fiscal rules, gilt yields can jump. That is exactly what happened in September 2022, when Reuters reported that two-year gilt yields rose nearly 50 basis points on the day of the mini-budget, and then another Reuters report showed them jumping as much as 54 basis points on 26 September alone.

And this is not ancient history. Reuters reported in July 2025 that policy U-turns had put fiscal worries back in focus, weakening the outlook for sterling and gilts. It also reported in February 2026 that concerns over Starmer’s future pushed longer-dated borrowing costs higher because markets were unsure whether a replacement would stick to current borrowing limits.

3) Interest-rate expectations

Politics also affects what markets think the Bank of England may need to do next.

A budget that looks inflationary can make investors expect slower rate cuts or even higher rates for longer. Reuters reported after Labour’s October 2024 Budget that gilt prices fell and markets trimmed expectations for Bank of England cuts, with 10-year yields hitting their highest level in a year.

That then ripples into the wider market. Higher expected rates can hit housebuilders, property shares, consumer stocks and any business that depends on cheap borrowing. Lower expected rates can do the opposite.

Recent events

The 2022 mini-budget: the clearest lesson of all

If you want one example of politics hitting markets hard, this is it.

Kwasi Kwarteng’s mini-budget in September 2022 combined large tax cuts with much higher borrowing and little reassurance on how it would all be funded. Reuters reported that sterling crashed to a record low, while gilt yields surged. The Bank of England then had to step in with temporary purchases of long-dated gilts to restore orderly market conditions and protect financial stability.

The key point is this: markets were not throwing a tantrum because they disliked one party. They were reacting to a loss of fiscal credibility. When Jeremy Hunt reversed most of the package in October 2022, Reuters reported that the pound and gilts soared. (Reuters)

The 2024 general election: politics as a stability event

Now flip to July 2024.

Labour’s landslide win was not treated as a market disaster. Quite the opposite. Reuters reported that UK assets gained, the FTSE 250 led the move, sterling rose modestly, and 10-year gilt yields fell. Investors saw the result as a reduction in political volatility after years of Brexit drama, leadership churn and the shadow of the mini-budget.

The October 2024 Budget: a test passed, but not perfectly

Labour’s first Budget also mattered. Reuters said it spared markets another “Liz Truss moment”. Sterling rose, the domestically focused FTSE 250 briefly jumped more than 1.5%, and the move in gilt yields was modest compared with 2022, even though bond markets still worried about borrowing and inflation.

That was a useful reminder that markets do not demand austerity at all costs. What they want is a sense that the numbers are credible, financed and under control.

Current backdrop

Today’s backdrop is a mix of domestic politics and global pressure.

Keir Starmer has been Prime Minister since 5 July 2024. In February this year concerns over his political position pushed UK borrowing costs higher and weakened sterling because markets started asking whether a new leader would keep the current borrowing framework. Reuters also reported later that month that sterling remained under pressure as traders speculated about change at Numbers 10 and 11.

What about the betting markets? They are worth watching, but only as sentiment gauges.

Oddschecker currently shows Reform at 13/8 and Labour at 11/4 in its “most seats” market for the next general election, with No Overall Majority at 7/10 and 2029 or later even money for the next election year. Meanwhile, Polymarket’s “Next UK Prime Minister in 2026?” market shows “No Next PM in 2026” at 52% and Angela Rayner at 20%, with $4.4 million traded.

I would read that this way:

- Bookmakers and prediction markets see political risk, but not a certain regime change

- The base case still looks like continuity, for now, which is a good thing.

- But markets are focusing on fiscal credibility, borrowing discipline and growth rather than ideology alone

What this means for investors

Do not build your portfolio around election guesses. That is usually a bad game.

A better approach is to watch the channels that tell you whether politics is becoming a real market problem:

- Sterling – is the pound being marked down?

- Gilts – are borrowing costs jumping relative to peers?

- FTSE 250 and domestic sectors – are UK-focused shares being repriced?

- Budget credibility – do markets believe the numbers?

For most long-term investors, especially those using ISAs and SIPPs, the sensible lesson is not to lurch in and out of the market on every headline. If you own a globally diversified portfolio, your returns will often be shaped more by the US, global growth, interest rates and energy prices than by Westminster alone. But if you have a heavy allocation to UK mid-caps, banks, housebuilders, property or domestic consumer shares, politics can matter more.

The bottom line

UK politics matters. But credibility matters more.

If you want to understand how politics is affecting markets, do not just stare at the FTSE 100 and ask which party is in charge. Look at the pound, gilt yields and the FTSE 250. That is usually where the real story is.

And the biggest lesson of all? Markets can live with political change. What they hate is uncertainty.