1) 📊 Last Week in Review

Week ending 29 May 2026

Performance snapshot (levels + weekly % + YTD):

- FTSE 100: 10,409 | -0.5% (YTD +6.6%)

- S&P 500: 7,580 | +1.4% (YTD +10.7%)

- MSCI World: 4,865 | +1.3% (YTD +10.7%, USD gross index variant)

- UK 10y gilt yield: 4.81% (-10 bp) | US 10y: 4.45% (-12 bp)

- GBP/USD: 1.3455 (+0.1%) | Brent: $92 (-1.7%)

What moved markets:

- AI optimism led again. The Nasdaq rose 2.4%, helped by strong AI infrastructure demand and a sharp move in Dell.

- Oil eased late in the week, calming inflation fears after Middle East ceasefire hopes briefly improved.

- Bond yields fell, with investors looking ahead to this week’s US jobs data and asking whether growth is slowing without breaking.

Sector & style:

- Best/Worst sector: US Information Technology +4.6% / Utilities -2.1%.

- Growth vs Value: Growth proxy won, with Nasdaq beating the S&P 500 by roughly 1.0 percentage point.

- Large vs Small: Small caps edged ahead, with Russell 2000 beating the S&P 500 by about 0.3 percentage points.

So what?

- Markets enter this week priced for a gentle slowdown, lower yields and still-strong AI spending.

- That makes US payrolls, services data and Broadcom earnings the main tests.

2) 🌟 The Defining Narrative

Can US jobs and AI earnings justify the rally without pushing bond yields back up?

Why it matters:

- Equity markets are leaning on a “soft landing” story: growth is slowing, but not collapsing.

- If jobs weaken gently, yields may stay contained and higher equity valuations can hold.

- If wages or services inflation reaccelerate, yields could rise again — a problem for expensive growth shares and global bond portfolios.

What confirms it / what breaks it:

- Confirms: US payrolls around expectations, calmer wage growth, contained ISM prices, and strong Broadcom AI guidance.

- Breaks: A hot jobs report, a jump in oil, sticky eurozone inflation, or weaker-than-expected AI demand.

UK investor angle:

- Global portfolios remain heavily exposed to the US technology cycle.

- Sterling moves matter: a stronger dollar can cushion overseas holdings in GBP terms, while a firmer pound can reduce translated returns.

3) 🏦 Central Bank Watch

Bank of England

- What’s scheduled: Andrew Bailey speech, Thursday 4 June, 16:40 UK; BoE Decision Maker Panel data, Friday 5 June, time not available.

- Market pricing: Bank Rate is 3.75%. The next MPC decision is due 18 June. Markets remain sensitive to whether inflation persistence forces a more hawkish path.

- Key thing to listen for: Any language on second-round inflation effects, especially wages and pricing behaviour.

- UK implications: Hawkish language would likely pressure gilts and support GBP; softer language would help duration-sensitive assets.

Federal Reserve

- What’s scheduled: Fed Beige Book, Wednesday 3 June, 19:00 UK; several Fed speakers through the week; no rate decision until 16–17 June.

- Market pricing: Fed funds target range is 3.50%–3.75%. Exact probability data not available.

- Key thing to listen for: Whether labour demand, wages and prices are cooling together.

- UK implications: US yields drive global discount rates. A higher US 10-year yield would be a headwind for global equities and bond funds.

European Central Bank

- What’s scheduled: Eurozone flash CPI, Tuesday 2 June, 10:00 UK; ECB speakers including Lagarde/Cipollone later in the week; next meeting 10–11 June.

- Market pricing: No exact probability data available; markets are focused on whether inflation keeps pressure on the ECB.

- Key thing to listen for: Core inflation and any sign that energy pressure is spreading into broader prices.

- UK implications: A hawkish ECB could lift European yields and weigh on GBP/EUR.

Bank of Japan

- What’s scheduled: Governor Ueda speech, Wednesday 3 June, time data not available; next BoJ decision 15–16 June.

- Market pricing: Exact probability data not available; markets continue to watch for a possible further rate increase.

- Key thing to listen for: Confidence that wage-led inflation is becoming durable.

- UK implications: BoJ policy affects global liquidity, Japanese equities and yen exposure in global funds.

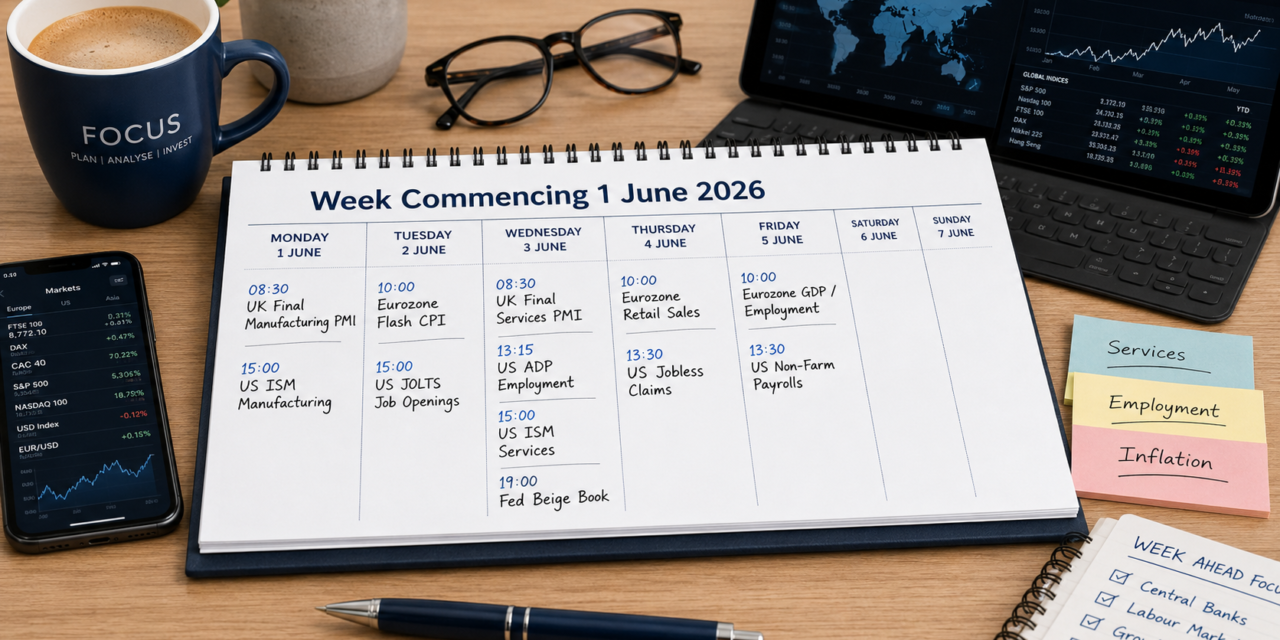

4) 🌍 Macro Calendar

| Day (UK) | Region & Event | Why it matters |

|---|---|---|

| Mon 1 Jun, 08:30 | UK Final Manufacturing PMI | Shows whether UK factories are absorbing higher costs or passing them on. |

| Mon 1 Jun, 10:00 | Eurozone Final Manufacturing PMI | A check on supply chains, energy pressure and export demand. |

| Mon 1 Jun, 15:00 | US ISM Manufacturing PMI | New orders and prices can move yields quickly. |

| Tue 2 Jun, 10:00 | Eurozone Flash CPI | Key inflation test before the ECB meeting. |

| Tue 2 Jun, 15:00 | US JOLTS Job Openings | Measures labour demand before Friday’s payrolls. |

| Wed 3 Jun, 08:30 | UK Final Services/Composite PMI | Services drive the UK economy, so this matters for BoE expectations. |

| Wed 3 Jun, 13:15 | US ADP Employment | A rough preview of payroll momentum. |

| Wed 3 Jun, 15:00 | US ISM Services PMI | The most important US activity release before payrolls. |

| Wed 3 Jun, 19:00 | Fed Beige Book | Gives on-the-ground evidence on demand, wages and prices. |

| Thu 4 Jun, 10:00 | Eurozone Retail Sales | Shows whether consumers are coping with higher living costs. |

| Thu 4 Jun, 13:30 | US Weekly Jobless Claims | A timely read on labour market stress. |

| Fri 5 Jun, time n/a | BoE Decision Maker Panel | UK business inflation and wage expectations feed into BoE thinking. |

| Fri 5 Jun, 10:00 | Eurozone GDP / Employment | Confirms the growth backdrop before the ECB meeting. |

| Fri 5 Jun, 13:30 | US Non-Farm Payrolls | The week’s biggest macro event for equities, bonds and FX. |

5) 📊 Earnings Watch

US

- Hewlett Packard Enterprise (HPE) — Monday:

- What matters: AI server demand, margins and enterprise IT spending will help test the wider AI infrastructure story.

- Palo Alto Networks (PANW) — Tuesday:

- What matters: Cybersecurity spending is a useful read on corporate technology budgets.

- Broadcom (AVGO) — Wednesday:

- What matters: The biggest earnings event of the week; investors want confirmation that AI custom chips and networking demand remain strong.

- CrowdStrike (CRWD) — Wednesday:

- What matters: Cloud security growth and customer retention will show whether premium software spending is holding up.

- Costco (COST) — Wednesday:

- What matters: A useful read on the US consumer and household spending resilience.

- Veeva Systems (VEEV) — Wednesday:

- What matters: Healthcare software demand gives a cleaner read on less cyclical technology spending.

- Lululemon (LULU) — Thursday:

- What matters: Premium consumer demand, China sales and margin guidance are the key lines.

UK

- British American Tobacco (BATS) — Tuesday:

- What matters: The pre-close update will focus on cash generation, debt, US cigarette trends and next-generation products.

Europe

- Inditex (ITX) — Wednesday:

- What matters: A major signal for global apparel demand, pricing power and supply-chain costs.

- Medtronic (MDT) — Wednesday:

- What matters: Healthcare equipment demand and margin guidance matter for defensive growth exposure.

6) 💷 Fixed Income & Currency Outlook

A) UK Gilts / Rates

- Facts: UK 2-year gilt yield ended around 4.22%, down roughly 12 bp on the week. UK 10-year gilt yield ended around 4.81%, down about 10 bp.

- View: Neutral. Yields look more attractive after recent volatility, but inflation and oil risks argue against aggressively extending duration.

- Watchlist: BoE speeches, UK services PMI, BoE DMP data, US payrolls and Brent crude.

- UK portfolio implication: Gilts can still diversify equity risk, but near-term returns remain sensitive to inflation headlines.

B) FX (GBP focus)

- Facts: GBP/USD ended around 1.3455, slightly higher on the week. GBP/EUR ended around 1.1537, slightly lower.

- View: Neutral / range-bound GBP. Sterling is caught between UK inflation risk, BoE caution and global dollar moves.

- Watchlist: US payrolls, eurozone CPI, BoE language and oil prices.

- UK portfolio implication: Unhedged global equity funds may still benefit if the dollar strengthens; GBP strength would trim overseas returns in sterling terms.

7) 🧠 Sentiment Check

- Current mood: Risk-on.

Market gauges:

- VIX / MOVE: VIX is around the mid-teens, signalling calmer equity markets. MOVE near 70 suggests bond volatility has cooled.

- Rates: US and UK 10-year yields fell last week, supporting growth shares.

- Credit spreads: Still tight, which suggests investors are not pricing much default stress.

- CNN FEAR & GREED INDEX: Current primary-source level not reliably available; broader market gauges are consistent with Greed / risk-on conditions.

Positioning / flows:

- Global equity funds saw modest inflows after the prior week’s outflow.

- US and European equity funds attracted money, while Asian equity funds saw outflows.

- Technology funds saw strong inflows, confirming that AI remains the dominant equity theme.

- Global bond funds also attracted sizeable inflows, showing demand for income and diversification.

Implication:

- Sentiment supports further upside if payrolls are benign and AI earnings hold up.

- The risk is that positioning has become too concentrated in the same AI winners.

8) 📈 Valuations & Expectations

Valuation snapshot:

- S&P 500 fwd P/E: 21.2x, above both its 5-year and 10-year averages.

Earnings expectations:

- Next-year EPS growth: FactSet’s CY2026 S&P 500 EPS growth estimate is 22.6%.

- Revisions trend: US revisions and earnings surprises remain supportive.

- Beat-rate context: Earnings season is thinner this week, but the remaining reports are important because Broadcom is a direct test of AI demand.

9) 🗳️ Geopolitics & Wildcards

- Event: Middle East tensions / Strait of Hormuz risk.

- Impact channel: Oil, shipping, inflation.

- What to watch: Any renewed strike, shipping disruption or collapse in ceasefire language.

- Most sensitive assets: Brent crude, airlines, inflation-linked gilts, GBP/JPY.

- Event: OPEC+ supply decision around the coming weekend.

- Impact channel: Oil supply and inflation expectations.

- What to watch: Whether any production increase is meaningful or mostly symbolic.

- Most sensitive assets: Oil, energy equities, inflation expectations.

- Event: UK gilt and fiscal sensitivity.

- Impact channel: Borrowing costs, sterling, domestic equities.

- What to watch: Any fiscal headlines, weak gilt auction demand or hawkish BoE language.

- Most sensitive assets: Gilts, GBP, UK banks, housebuilders.

- Event: AI earnings concentration.

- Impact channel: Equity valuations and risk appetite.

- What to watch: Broadcom and CrowdStrike guidance.

- Most sensitive assets: Nasdaq, semiconductors, global technology funds.

10) ⚡ The Bottom Line

- If US payrolls are soft-but-not-scary → then yields may stay capped and global equities can extend gains → watch the US 10-year around 4.50%.

- If oil or eurozone CPI surprises higher → then inflation fears return and gilts could sell off → watch Brent around $95–$100 and the UK 10-year near 4.90%.

- If Broadcom or CrowdStrike disappoints → then AI leadership could wobble and growth stocks may underperform → watch Nasdaq versus the S&P 500.

© Clearly Investments Ltd. Educational information only. This is not investment advice.