Gold has had many advocates over the centuries, but the arguments for owning it today are more specific, than at any point in recent history. Forget the vague appeals to “store of value” or inflation hedging. There are three, interconnected reasons why a meaningful allocation to gold belongs in every serious portfolio.

Reason One: Gold Is the Unfreezable Asset

In February 2022, the Western financial system demonstrated something that changed the thinking of central banks, sovereign wealth funds, and institutional investors around the world: it rendered hundreds of billions of dollars of reserves worthless with the click of a button.

When the US and EU jointly froze approximately $300 billion of Russia’s foreign exchange reserves following its invasion of Ukraine, they immobilised the bulk of Russia’s $600 billion reserve stockpile overnight. US Treasuries, euro-denominated bonds, dollars held in foreign accounts — all of it became inaccessible, because every one of those assets was controlled by the governments that had imposed the sanctions. The roughly $120 billion Russia held in physical gold, stored in domestic vaults, remained entirely untouched.

“The West demonstrated that it could render $300 billion of reserves worthless overnight. Physical gold held domestically is the one reserve asset that cannot be frozen.”

This was not a theoretical risk — it happened. And it forced every government, central bank, and large institutional investor to ask the same question: which of our assets can be frozen?

Gold’s answer is unique among all major asset classes. It is physical. It can be moved outside digital financial networks. It carries no counterparty risk — there is no liability on the other side of the trade. It can be stored, transported, and exchanged entirely outside the global banking networks.

The real-world evidence of this goes beyond Russia. Venezuela’s government, cut off from global finance by successive waves of US sanctions, flew gold bars to Uganda, the UAE, and Turkey, exchanging them for cash euros to fund imports. Iran accepted gold from Venezuela as payment for oil refinery repairs, bypassing financial markets.

This is not lesson is not about sanctions — it is about counterparty risk. Every bond, every equity, every ETF, every bank deposit involves a counterparty. Physical gold does not. In a world of rising geopolitical tensions, that physical property has a real and growing value. The 2022 freeze was a watershed. The era of assuming your assets are safe simply because they are legally yours is over.

Reason Two: Central Banks Are Devaluing Their Currencies — and Buying Gold to Prove It

The second reason to own gold is government debt. The world’s major governments — including the UK and the US — are running deficits that are increasing every year. The US federal debt has exceeded $36 trillion. The UK runs a deficit. Japan’s debt-to-GDP ratio is above 250%. The mechanism by which these debts are ultimately resolved is almost always the same: the value of the currency is effectively reduced over time.

Gold has been the historically reliable hedge against this process. It cannot be printed. Its above-ground stock grows by only 1.5–2% per year as new mine is added — roughly in line with global economic growth, and far below the rate at which modern governments expand their money. This scarcity is geological. And it is precisely why central banks themselves, the very institutions responsible for managing currencies, have been buying gold.

Central banks purchased over 1,000 tonnes of gold per year in both 2022 and 2023 — roughly double the historical average. China has been adding to its reserves consistently for over a decade, accumulating nearly 900 tonnes between 2009 and 2021, and continuing its buying streak for 14 consecutive months through late 2025. Poland, India, Turkey, and a string of Middle Eastern nations have all been active buyers. Their motivation is transparent: they are reducing their exposure to the US dollar as the world’s dominant reserve currency, and gold is the only alternative reserve asset that exists outside any nation’s control.

“Central banks are the world’s largest currency managers. When they sell bonds and buy gold at record pace, they are telling you something about what they think their own currencies are worth.”

The other tailwind in 2025 is real interest rates. Real interest rates — are the most important short-term driver of the gold price — these fell significantly as the Federal Reserve cut rates multiple times in 2025. For UK investors, the sterling dimension adds an additional layer: a weakening pound — a recurring feature of British economic life — amplifies gold returns in sterling terms.

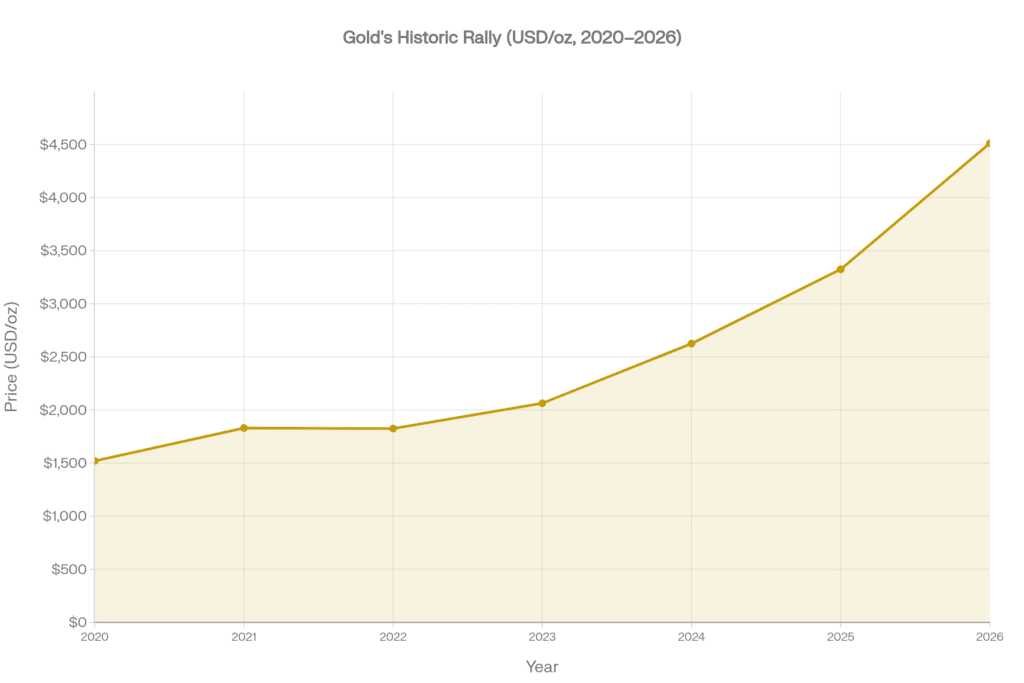

Gold’s 2025 performance — a 60% rise, its best year since 1979 — was a market response to a world in which the institutions responsible for issuing paper money are, through their own buying behaviour, demonstrating that they don’t fully trust it.

Reason Three: The World’s Asset Allocators Have Barely Started Buying

The third reason is perhaps the most powerful — and the least appreciated. It is a story about market structure, relative size, and the potential impact of a modest change in behaviour by the world’s institutional investors.

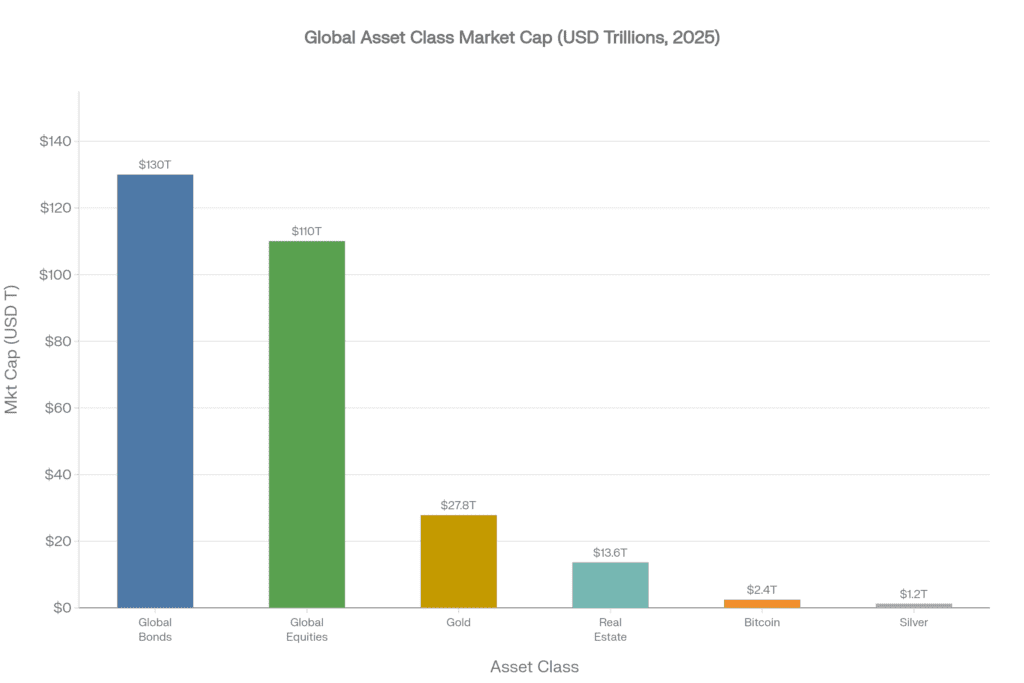

Start with scale. Gold’s total market capitalisation now exceeds $27.8 trillion, making it larger than any single national equity market. Yet this number, impressive as it sounds, is small in the context of global capital markets. Global equities are worth approximately $110 trillion. Global bonds represent around $130 trillion. The entire gold market — every gold bar, coin, ETF unit, and futures contract in existence — is worth roughly one quarter of global equities.

Now consider this: gold mining equities currently represent just 0.39% of total world equity market capitalisation. At the 2011 gold bull market peak, that figure was 0.71%. A return to that share alone would require enormous capital inflows into mining stocks. But more broadly, most global institutional portfolios — pension funds, insurance companies, sovereign wealth funds, endowments — carry gold allocations of 0–2%.

“The entire gold market is worth one quarter of global equities. If the world’s institutional asset allocators shifted just 3% of their equity portfolios into gold, they would need to buy the equivalent of several years of total global mine production.”

The mathematics of this potential demand shift are important. If global asset managers were to increase their gold allocation from 1% to just 4% of assets — the demand they would generate would exceed the annual supply of newly mined gold. With mine production running at roughly 3,672 tonnes per year, the price impact would be significant.

This reallocation is already beginning. Global gold ETF holdings grew by 801 tonnes in 2025 — the second strongest year on record — as Western institutional money returned to the market after significant outflows in 2022–23. Bar and coin demand hit a 12-year high as retail investors simultaneously sought tangible wealth preservation. ETF products such as iShares Physical Gold ETC (IGLN) and Invesco Physical Gold ETC (SGLD), listed on the London Stock Exchange and fully eligible for Stocks & Shares ISAs, have made gold more accessible and tax-efficient for UK investors than ever before.

The structural case for ETF-driven inflows is compelling. A generation of investors now have an easy low-cost way to own gold , with ISA-eligible products costing as little as 0.12% per year. As awareness of gold’s portfolio properties grows — driven by the 2022 sanctions, persistent inflation, and fiscal concerns — the pool of potential buyers will grow.

What This Means for Your Portfolio

For UK investors, the practical implications are straightforward:

- Start with a gold ETF in your ISA — IGLN or SGLD on the London Stock Exchange, costing 0.12–0.25% per year, fully CGT-free within the ISA wrapper

- Consider physical coins for longer-term wealth preservation — Royal Mint Britannias and Sovereigns are CGT-exempt as UK legal tender, making them uniquely efficient for high earners

- For leveraged exposure — gold mining equities (Barrick, Newmont) and royalty companies (Franco-Nevada, Wheaton Precious Metals) offer geared participation in rising gold prices, with the added benefit of dividends

- Target a 5–10% portfolio allocation — even a 2.5% position measurably improves the overall risk ratio of a diversified portfolio

Gold is not a trade. It is not a bet on chaos. It is the response to a world in which digital assets can be frozen, currencies are being gradually debased, and the world’s largest pools of capital are only beginning to reflect that reality in their portfolios.