Investing can be difficult, especially in a period of 24 hour news and the press knowing bad news headlines receive more attention.

So what can investors do? We have used the benefit and experience of many years of investing to provide 6 lessons, to help explain how makets react to events, and what you should do about it.

Need-to-knows

- If it is in the news, it is often already in the price. Public information is absorbed fast.

- Markets anticipate events. They price what they think is coming, not just what has just happened.

- The move depends on expectations. A “good result” can still send a share price down if investors expected even more.

- Forward guidance usually matters more than the last quarter. Markets care more about the next 12 months than the last 12 months.

- Uncertainty and flows can exaggerate moves. In stressed markets, investors often price in extra risk, and systematic or retail flows can push prices further than fundamentals alone would suggest.

If it is in the news, it is in the price

This is the hardest lesson for private investors to accept. By the time a headline hits your phone, it has usually already hit trading desks, algorithms, institutional investors and professional news feeds. The first move is often gone. Research found that several effects of public news are completed within the first minute. That does not mean every price move is perfect. It means the easy, obvious reaction is usually not there for long.

Think about a company trading update usually these happen very early. By the time you read the news summary, analysts have already compared the number with forecasts, adjusted profit assumptions, and repriced shares, bonds or currencies. It is the same with global and political events, if you are watching it, there is no need to be concerned about future price movements, it has already happened.

Markets don’t react to events. They anticipate event

Markets are not just waiting for events to happen. They are trying to price what they think will happen next. That is why company guidance matters so much. When management raises, cuts or reaffirms guidance, it changes analysts’ models for future revenues, margins and profits. When reading the financial press earnings coverage routinely focuses on whether firms reaffirm or change guidance, because that shapes expectations, not just the quarter that has already gone.

This is also why scheduled events are often partly priced in before they happen. Central-bank meetings, CPI releases, payrolls data and company earnings dates are all known in advance. Investors position for the probabilities beforehand. Markets are not merely reacting to the event. They are trading the gap between the event and what was already expected.

Ryanair is a good example of markets anticipating the news rather than waiting for the official moment. The low point in the share price during COVID, was 18th March 2020, which was before Boris Johnson, announced the lockdown on 23rd March. So whilst you may have thought the lockdown announcement was a time to sell the shares, actually this was a buying signal. The share rallied over 50% in a matter of months. But many investors though differently and sold.

The move depends on what markets were expecting

This is where many investors get tripped up. They think “good news should make shares go up.” Not necessarily. Markets do not compare reality with zero. They compare reality with expectations. If expectations were already sky-high, even strong results may disappoint. If expectations were gloomy, merely “less bad” can be enough to lift prices.

So do not ask, “Was this good or bad?” Ask, “Was it better or worse than the market expected?” That is the question prices answer.

A recent exaple was earlier this year , Nvidia delivered better-than-expected results and forecast revenue above analysts’ estimates, yet the shares still fell. Investors looked past the headline beat and worried about whether the huge AI spending boom would deliver enough future returns, and whether competition would rise. That is a perfect example of markets reacting not to the number itself, but to the gap between results, expectations and future confidence.

Markets are pricing the future, not the past

The news talks about what has happened, but a share price is not an indicator for what a business achieved last year. It is a valuation of what investors think that business can earn in the future, discounted for possible risks.

You are setting the price for receiving the future profit of the company for the next 5,10 or 20 years. That is why markets often care more about the statement on current trading, the margin outlook, or the revenue guidance than the historical results section. Changes in expectations about future cash flows and required return are what matter for market values.

This is also why two companies can report similar results and get completely different share-price reactions. One might sound confident about the year ahead. The other might sound cautious. The market will normally give more weight to the forward view.

An example of this played out in April 2026 when Netflix reported its quarterly earnings. The results were strong — revenues were up, subscriber numbers were healthy, and the business was performing well. Yet the share price fell.

Because Reed Hastings, the company’s co-founder and a towering figure in its story, announced he was stepping down from the board. In an instant, the market looked straight past the strong backward-looking numbers and asked a forward-looking question: what does this company look like without the vision and credibility of its founder? That uncertainty was enough to outweigh an impressive set of financials. This is markets doing exactly what they always do: ignoring the past results and pricing in what they believe comes next.

It‘s not the news, it’s the uncertainty

Bad news is one thing. Uncertainty is another. In markets, uncertainty often matters even more because uncertainty raises the return investors demand for holding risk. In simple terms, investors pay less for an asset when they are less sure about the future.

That is why markets can overshoot after bad news. Analysts are not just cutting earnings forecasts. They may also be widening the range of possible outcomes and demanding a bigger risk premium. Recent work on belief overreaction also argues that investors can overreact to news, increasing the market falls.

The Iran conflict shows that markets often price uncertainty more aggressively than the news itself. As the risk of a wider war grew, investors had to consider a whole range of outcomes: higher oil prices, supply disruption through the Strait of Hormuz, more inflation pressure, and fewer interest-rate cuts. The lesson is markets are constantly repricing the probabilities as uncertainty rises and falls, which is why the biggest moves often come from changing expectations rather than from the final outcome itself.

Flows of money push markets too

Not every market move is driven by news . Sometimes markets move simply because large pools of money are forced to trade — regardless of what is happening in the world. Two strategies are particularly important here: trend-following funds (which buy rising assets and sell falling ones, following price momentum with no fundamental judgement whatsoever) and risk-parity funds (which automatically reduce their positions as volatility rises, to keep portfolio risk constant).

Together, these systematic strategies manage hundreds of billions of dollars globally. When markets fall, volatility spikes, which forces risk-parity funds to sell, which pushes markets lower still, which raises volatility further.

In particular we saw this during the COVID crash of March 2020, the where volatility-targeting strategies “contributed to price movements” — with some funds required to sell positions equivalent to multiples of their capital, not because of any view on the world, but simply because an algorithm told them to.

The lesson for investors: in a sharp sell-off, a significant portion of the selling you see is not human judgement — it is machines following rules. That mechanical selling can make markets look far worse than the underlying reality justifies, and it should make you less likely to panic alongside them, not more.

So what should you do?

Only act when you think you have an information advantage

That is the real lesson.

If markets are moving violently, headlines are flying, and everyone is staring at the same news feed, your information advantage is probably very small. In those moments, doing less is often the better decision.

This is also where overtrading and overconfidence becomes expensive. Some interesting research called Boys Will Be Boys, Barber and Odean found that men traded more than women, and that the heavier trading hurt returns. Their central point still matters today: overconfidence leads to excessive trading, and excessive trading damages performance.

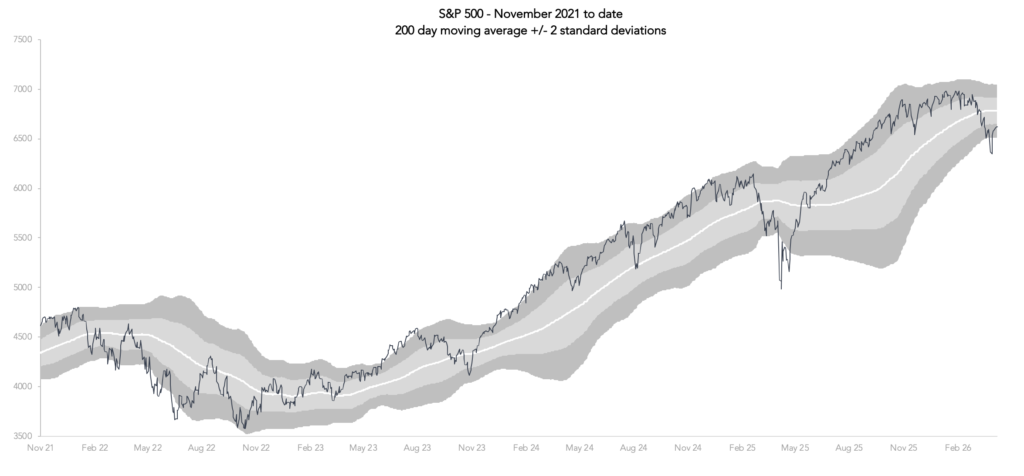

A practical indicator: Bollinger Bands

There will be opportunities, from extreme market moves, one simple tool some investors use to judge whether a move looks stretched is Bollinger Bands.

Bollinger Bands are a simple way of showing whether a share price looks normal or stretched compared with its recent trading range. They use a moving average (200 days moving average is shown in the chart), with an upper and lower band set around it, and the bands widen when markets are more volatile and narrow when markets are calmer. In practice, if a share price is pushing up towards or beyond the upper band, it may suggest the move has become extended; if it is falling towards or below the lower band, it may indicate the sell-off is unusually sharp.

That does not make Bollinger Bands a buy or sell signal, because strong trends can stay near the bands for some time, but they are useful as a discipline tool to help investors recognise when a move looks extreme.

What this means for investors

The smartest question is usually not, “What is the news?”

It is: “Do I genuinely know something the market has not already worked out?”

If you do feel compelled to act on market volatility remember the Warren Buffet quote, “Money is like a bar of soap the more you touch it, the less you’ll have.”

Past performance and historical patterns are not a guarantee of future returns. This article is intended for general information and educational purposes and does not constitute financial advice. Always seek independent financial advice before making investment decisions.