An ISA (Individual Savings Account) is simply a tax-free savings or investment account. Any interest, dividends, or capital gains you earn inside an ISA are completely free from income tax and capital gains tax (CGT), as long as the money stays inside the wrapper.

You don’t need to declare ISA income or gains on a self-assessment tax return, which simplifies your financial admin considerably.

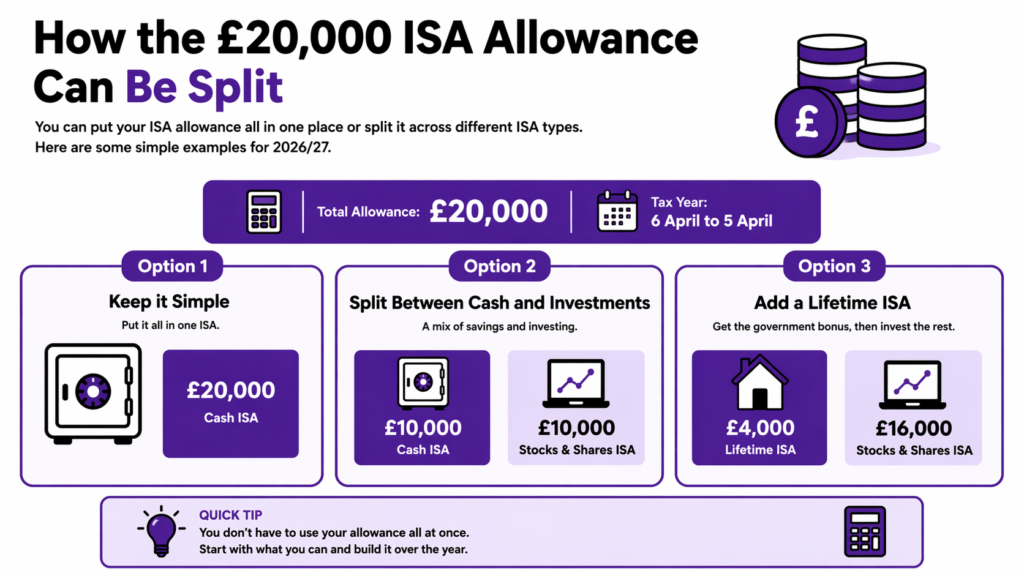

For the 2026/27 tax year, the overall adult ISA allowance remains £20,000. One important future change is already confirmed: from 6 April 2027, the annual Cash ISA limit for people under 65 will be £12,000, while savers aged 65 and over will still be able to put up to £20,000 into a Cash ISA each year.

Need-to-knows

The adult ISA allowance is £20,000 in the 2026/27 tax year.

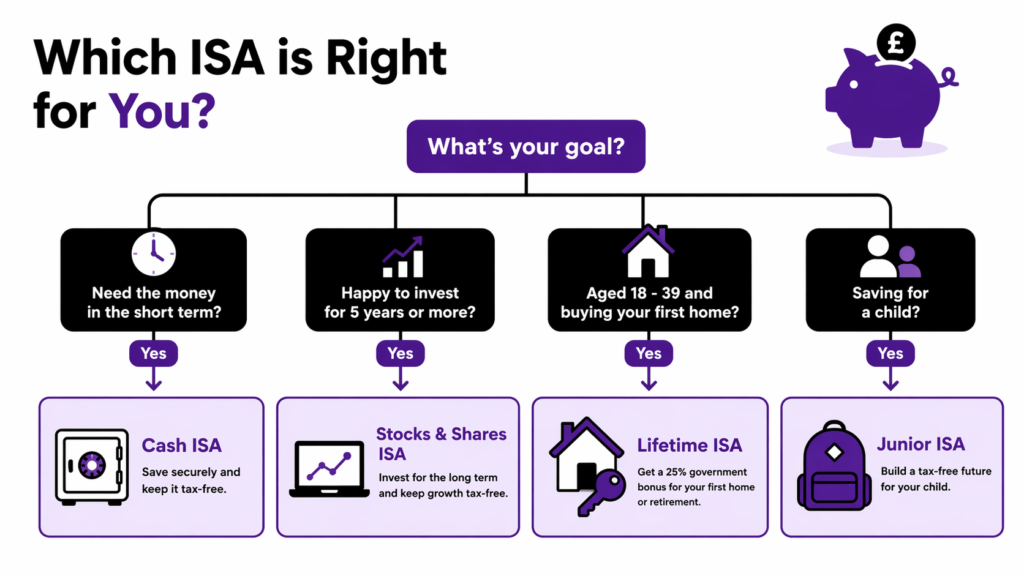

The main adult ISA types are Cash ISA, Stocks and Shares ISA, Lifetime ISA and Innovative Finance ISA.

A Junior ISA is available for children, with a £9,000 annual limit in 2026/27.

A Lifetime ISA lets eligible savers put in up to £4,000 a year, with a 25% government bonus.

You can split your ISA allowance across different ISA types.

The different types of ISA

Cash ISA

A Cash ISA is simple. You deposit cash, earn interest, and that interest is tax-free inside the wrapper. It is usually best suited to short-term money, emergency funds, or anyone who values certainty over grow.

Cash ISAs come in different forms, including easy access and fixed rate versions. Fixed rates can be useful, but one common mistake is doing nothing when the fixed deal ends. Once the fixed period expires, the rate may become much less competitive, so it is worth reviewing your options rather than letting the money drift.

Watch out: a fixed-rate Cash ISA can become a poor home for your cash once the fixed term ends.

Stocks and Shares ISA

A Stocks and Shares ISA is for longer-term investing. Instead of simply earning savings interest, your money is invested. That gives you the chance of better long-term growth, but it also means the value can fall as well as rise.

A very important point is this: a Stocks and Shares ISA does not automatically mean high risk. The level of risk depends on what you hold inside it.

What can you hold inside it?

Inside a Stocks and Shares ISA, you will commonly find:

- investment funds

- ETFs

- investment trusts

- individual shares

- bond funds

- government bonds or gilt exposure

- cash

- money market funds

If you want to take less risk, a Stocks and Shares ISA can still work. Rather than stocks and shares you can buy government bonds or money market funds for more cautious approach. See our articles on Government Bonds.

Lifetime ISA

A Lifetime ISA can be used either for buying a first home or for later life. You must be age18 to 39 to open one, and you can contribute up to £4,000 a year until age 50. The government adds a 25% bonus, worth up to £1,000 a year.

| Feature | Details |

|---|---|

| Annual contribution limit | £4,000 (counts towards your £20,000 ISA allowance) |

| Government bonus | 25% — up to £1,000 per year |

| Age to open | 18–39 |

| Contributions until | Age 50 |

| Maximum lifetime bonus | £32,000 (on £128,000 of contributions) |

| Eligible withdrawals | First home purchase or retirement (age 60+) |

| Early withdrawal penalty | 25% charge (effectively a 6.25% loss on your own money) |

This can be a very attractive option for eligible first-time buyers. But there is a catch: if you take money out for a reason that does not meet the rules, a withdrawal charge normally applies.

Junior ISA

A Junior ISA is a tax-free account for a child under 18. In 2026/27, up to £9,000 can be paid in. A child can have a cash Junior ISA, a stocks and shares Junior ISA, or both.

This can be a way for parents and grandparents to build long-term savings for a child in a tax-efficient way.

How the ISA allowance work

For the 2026/27 tax year, the adult ISA allowance is £20,000. You can put it all in one place, or split it across different ISA types.

You can split your annual allowance across different ISA types, and current rules allow much more flexibility than many people realise. One important exception is the Lifetime ISA, where you can only pay into one Lifetime ISA in a tax year, with a maximum contribution of £4,000. The key point is the total amount, not the number of accounts you hold.

Some ISAs are flexible. That means if you can withdraw money and then put it back in during the same tax year, as long as you remain within the allowance. This is a great way to have tax free interest on your day to day savings.

| ISA Type | 2026/27 Limit | Age to Open | Savings at Risk? | Government Bonus? |

|---|---|---|---|---|

| Cash ISA | £20,000* | 18+ | No | No |

| Stocks & Shares ISA | £20,000* | 18+ | Yes | No |

| Lifetime ISA | £4,000 (within £20k) | 18–39 | Depends | Yes – 25% |

| Innovative Finance ISA | £20,000* | 18+ | Yes | No |

| Junior ISA | £9,000 | 0–17 | Depends | No |

* The £20,000 is a combined limit across all adult ISAs. Cash ISA limit reduces to £12,000 from April 2027 for under-65s.

Transferring ISAs

You can transfer ISAs between providers without losing your tax-free status. The important rules are:

– Always use a formal ISA transfer — never withdraw money and re-deposit it, as this uses up your current year’s allowance

– You can transfer current year contributions as well as previous years’ accumulated ISA savings

– You can transfer from one ISA type to another (e.g., a Cash ISA into a Stocks & Shares ISA)

– There is no limit on how much of your accumulated ISA pot you can transfer

– Junior ISA to Junior ISA transfers are also permitted and do not count towards the annual allowance

Biggest ISA mistakes to avoid

- If you want to move an ISA to another provider, use the official ISA transfer process. Do not simply withdraw the money yourself and pay it back in elsewhere.

- Consider and compare charges

- Forgetting to use your allowance before the tax year ends

- Not understanding what is inside your Stocks and Shares ISA

- Not reviewing a fixed-rate Cash ISA when the deal expires

The budget change to know about

For 2026/27, the overall adult ISA allowance is still £20,000. But from 6 April 2027, the annual Cash ISA limit for people under 65 will be £12,000, while people aged 65 and over will still be able to put up to £20,000 into a Cash ISA. The overall ISA allowance remains £20,000

Final thoughts

ISAs are one of the most useful tools available to UK savers and investors.

For short-term money, cash may make sense. For long-term money, investing may be more suitable. For first-home buyers, the Lifetime ISA can be powerful. And for families, the Junior ISA can be a useful long-term gift.

This guide is for educational purposes and does not constitute personalised financial advice. Tax rules can change and their impact depends on your individual circumstances. Always consider seeking independent financial advice if you’re unsure about the best ISA strategy for your situation.