Investing in the right way is important, but putting the right structure in place, is even more important.

If I were advising a client, I wouldn’t start with “the best fund” or “the hottest investment idea”.

I would start with the questions that are really important: how much cash you need, are you using your tax allowances, what are you saving or investing for, what if something happens to you, and when can you retire.

So these are the 10 things a professional adviser would most likely tell you to think about.

This is for UK based investors, and whilst it is not personal financial advice, it is for you to think about.

Need-to-knows

Use a your ISA allowance of £20,000 in 2026/27, and Junior ISAs remain £9,000.

A Lifetime ISA still allows up to £4,000 a year, with a 25% government bonus, for eligible adults.

Pension tax relief is still one of the biggest wealth-building tools: for most people the annual allowance is up to 100% of earnings or £60,000, whichever is lower.

UK investors now need to watch the much smaller tax shelters: the CGT annual exempt amount is £3,000 and the dividend allowance is £500 in 2026/27.

Estate planning matters more than many people realise: the IHT nil-rate band is £325,000, the residence nil-rate band is £175,000, and HMRC says these are fixed until 5 April 2031. The annual gift allowance is £3000.

1) 💰 Build a cash reserve before you invest

The first thing I would tell you is simple: do not invest money you may need soon.

Before you put money into the stock market, make sure you have a sensible emergency fund in place. That usually means cash for unexpected costs, short-term spending plans and any known big expenses coming up over the next few years.

Many people I have seen who have lost money in markets have had to sell at the wrong time.

Why this helps you

If your emergency cash is in place, you are less likely to sell investments at the wrong time. This helps you stay invested for the long term.

2) Use your ISA allowance properly

For most UK clients, I would say: use your ISA allowance as fully as you sensibly can.

A Stocks and Shares ISA is one of the best ideas available because income and gains are sheltered from tax. A Cash ISA can also be useful for money that needs to stay secure. The point is to have a bigger part of your money free fromn tax over time. Otherwise you are paying away part of your income and gains.

Why this helps you

More of the return stays in your pocket.

3) Make full use of your pension

A professional adviser would almost certainly tell you this: do not ignore your pension.

Pensions remain one of the most effective long-term wealth-planning tools in the UK because of tax relief and, for many people, employer contributions. If you are employed, one of the first questions is whether you are getting the full employer match. If you are self-employed, the question becomes whether you are using pension contributions enough.

You may also want to think about whether a SIPP gives you more control over how your retirement money is invested.

Why this helps you

Pensions can help you build wealth faster because tax relief boosts the value of what goes in. This is one of the simplist ways to reduce your tax bill.

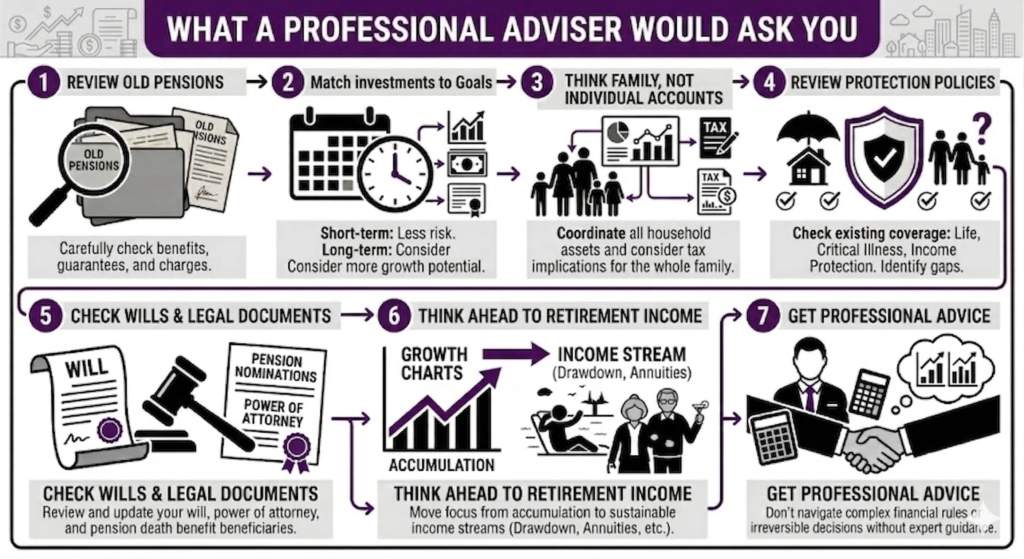

4) Tidy up old pensions — but do not move the wrong one

Many clients I have seen, have pensions scattered across old employers and providers. I would often tell a client to review them and simplify where it makes sense.

You can’t monitor and manage numerous schemes, and you don’t know if every scheme is doing the right thing for you.

But I would also give a strong warning: not every pension should be moved. Some older schemes may contain valuable guarantees or defined benefit rights. These can be far more valuable than they first appear.

Why this helps you

Done well, consolidation can mean less paperwork, lower charges and a clearer retirement picture. Think about managing drawdwon multiple schemes. But done badly, it can mean giving up benefits you cannot get back.

5) 📈 Match your investments to your goals, not to headlines

One of the most important things I would tell you is this: your investment plan should reflect your life, not the news cycle.

Your money may have different objectives or goals. Some of it may be for retirement in 15 years. Some may be for helping children later on. Some may need to produce income sooner. Those different goals may need different levels of risk and different products.

A good plan usually starts with:

- What the money is for?

- When you will need it?

- How much risk you can realistically take?

- How much volatility you can emotionally tolerate?

Why this helps you

When the markets do fall you have a plan, you can stick to. And if you can stick to the plan you will see those longer term returns.

6) 🏡 Think about the whole family, not just your own accounts

A professional adviser would not just look at your accounts in isolation. They would usually look at the wider household.

That may mean thinking about:

- Whether both of you are using their ISA and pension allowances

- Whether savings or investents should be held in one name or split across both

- Whether Junior ISAs or other long-term savings for children are appropriate

- If you can use both partners Capital Gains Tax Allowances

Why this helps you

Your allowances are pretty small these days so think about other members of the family. If you move investments between married partners, you do not pay any capital gains.

7) Plan now for how you will take your income in retirement

Saving is only half the job. At some point, you may need to turn it into income.

That is why you should think about retirement income, even if retirement still feels a long way off. Later on, the key questions often become:

- How much income do you want?

- Should you draw from pensions, ISAs or taxable investments first?

- How do you take money without creating unnecessary tax?

This is really important, because many investment schemes, will reduce the risk as you head towards retirement, but hopefully you should be using thins money for the next 10, 20 years or even longer. So it may be right to reduce the risk of some of the money, but not all.

Why this helps you

How you decide to do this, will tell you how you manage your money for the years leading up to retirement and can make a big difference. I know, I have seen it happen.

8) Protect the plan, not just the investments

A lot of people focus only on growing wealth. A professional adviser would remind you that you should be protecting yourself too.

That may mean discussing products such as:

- life cover

- income protection

- critical illness cover

These are not exciting. But they can be incredibly important. If your income stopped tomorrow, or something happened to you, would your family still be financially secure?

Why this helps you

Protection products help stop one illness, accident or death from derailing your plan. Just ask your self the question, what would i do if something happened.

9) Get your estate plan in order

If I were advising you, I would not stop at investments and pensions. I would also want to know whether your estate planning is in order.

That means looking at things such as:

- your will

- pension beneficiary nominations

- gifting strategy

- powers of attorney

- whether trusts may be appropriate in more complex cases

This is really complex, and also difficult from a family point of view, but just discuss this and have an idea.

Why this helps you

Estate plans, usually mean doing a number of different things, gifting, trusts, life assurance, accepting you will pay some Inherritance tax. See our article on Inheritance Tax planning.

10) Decide when to do it yourself and when to get professional advice

This is the honest answer a good adviser should give you.

Some things you can do yourself. If your finances are straightforward, you may well be able to manage basic saving, simple ISA investing and regular pension contributions without ongoing professional help.

But when things become more complex, advice becomes much more valuable. That is especially true for areas such as:

- retirement planning

- protection

- more complicated tax planning

- pension consolidation where valuable benefits may be involved

- estate planning

- later-life income decisions

Why this helps you

You avoid paying for help you do not need, but you also reduce the risk of making a mistake in the areas where expert advice can add real value.

Your checklist

- List everything you have: cash, ISAs, pensions, investments, mortgages, insurance and wills.

- Separate short-term money from long-term money.

- Check whether you are using your ISA and pension allowances well.

- Review old pensions carefully before moving anything.

- Make sure your investments match your timescales.

- Think about the family, not just individual accounts.

- Review what protection you do and do not have.

- Check your will, nominations on any pensions and powers of attorney.

- Think ahead to retirement income, not just accumulation.

- Get advice where the decisions are more complex or more permanent.