As interest rates remain higher than they have been for a number of years, many savers are finding themselves in a position they haven’t been in for years: actually owing tax on their bank interest.

If you have a tidy sum in a standard savings account, it’s vital to check if you’re about to hand a slice of that hard-earned interest back to HMRC. Here is the full lowdown for the 2026/27 tax year.

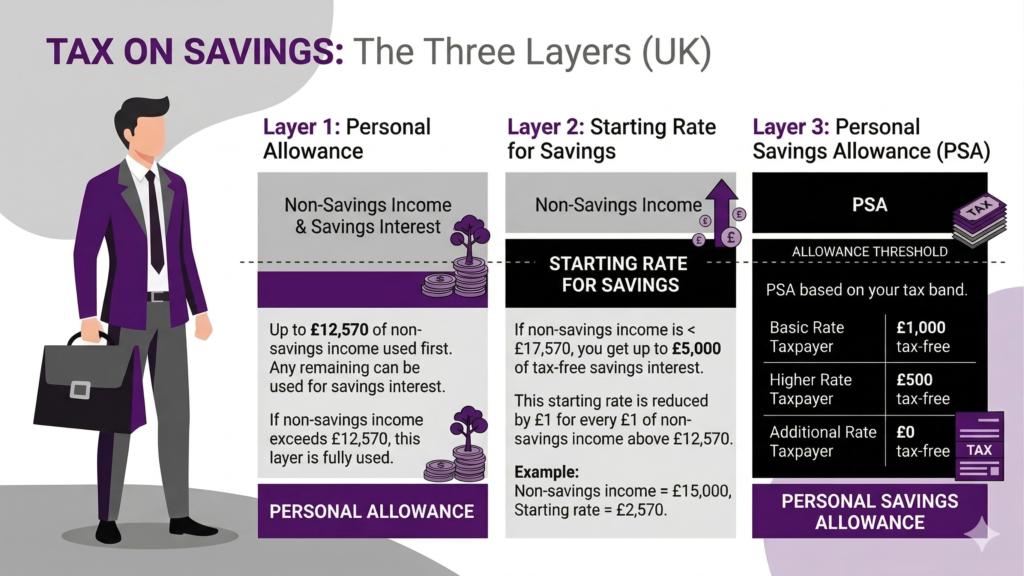

1. The Savings Allowance

Before HMRC takes a penny of your savings interest, you actually have up to three separate layers of tax-free allowance working in your favour.

Layer 1: The Personal Allowance (£12,570)

Everyone in the UK gets a Personal Allowance of £12,570 per year — the amount you can earn completely free of income tax. If your wages, pension, or self-employment income doesn’t fully use up this allowance, the leftover portion can shield savings interest. This typically only benefits people with very low other income.

Layer 2: The Starting Rate for Savings (up to £5,000 at 0%)

This is a little-known bonus for lower earners. If your non-savings income (wages, pension, etc.) is below £17,570, you may be eligible for a 0% tax rate on up to £5,000 of savings interest. But for every £1 your other income exceeds the £12,570 personal allowance, this band shrinks by £1. So if you earn £17,570 or more from wages, this benefit disappears entirely.

| Other Income | Starting Rate Band Available |

|---|---|

| £12,570 or less | Full £5,000 |

| £14,570 | £3,000 |

| £16,570 | £1,000 |

| £17,570 or more | £0 |

Layer 3: The Personal Savings Allowance (PSA)

This is the big one that affects most people. Your Personal Savings Allowance is the amount of savings interest you can earn each year without paying any tax, on top of your other allowances. The amount depends on your income tax band:

| Tax Band | Income | Personal Savings Allowance |

|---|---|---|

| Non-taxpayer | Up to £12,570 | £1,000 |

| Basic rate (20%) | £12,570 – £50,270 | £1,000 |

| Higher rate (40%) | £50,270 – £125,140 | £500 |

| Additional rate (45%) | Over £125,140 | £0 |

Once your savings interest exceeds your PSA, the excess is taxed at your marginal rate — 20%, 40%, or 45%. Importantly, your PSA is based on the highest rate of tax you pay, not the average. So if your income tips you into higher-rate territory — even by £1 — your PSA halves from £1,000 to £500

2. Examples of how this works

To understand all of these numbers, lets look at a few examples, let’s assume you are using a top-tier easy-access savings account paying 4% interest.

The Basic Rate Payer (Earning £30,000)

- Allowance: £1,000.

- Scenario A: You have £20,000 in savings.

- Interest earned: 20,000 × 4% = £800.

- Tax Due: £0 (It’s under your £1,000 limit).

- Scenario B: You have £40,000 in savings.

- Interest earned: 40,000 × 4% = £1,600.

- The first £1,000 is tax-free. You pay 20% tax on the remaining £600.

- Tax Due: £120.

The Higher Rate Payer (Earning £60,000)

- Allowance: £500.

- Scenario A: You have £10,000 in savings.

- Interest earned: 10,000 × 4% = £400.

- Tax Due: £0 (It’s under your £500 limit).

- Scenario B: You have £40,000 in savings.

- Interest earned: 40,000 × 4% = £1,600.

- The first £500 is tax-free. You pay 40% tax on the remaining £1,100.

- Tax Due: £440.

3. An option for High Earners: Low-Coupon Government Bonds

If you have used your ISA allowance and your Personal Savings Allowance, Government Bonds (Gilts) are the most tax-efficient place for your cash in 2026.

UK Gilts have a unique tax status: the interest (coupon) is taxable, but any capital gain is 100% tax-free.

The Strategy

Look for “low-coupon” gilts. These were issued when rates were low and now trade at a discount. For example, you buy a bond for £95 that will pay you £100 in a year’s time.

- The interest payment might be tiny (e.g., 0.25%), so you pay almost no income tax.

- The £5 profit (the gain from £95 to £100) is a capital gain.

- On a Gilt, that £5 profit is tax-free, even if you’re an Additional Rate payer.

See our articles on Government Bonds. You can find a list of Government Bonds, and current yields here.

4. Recommendations: How to keep more of your interest

To ensure you keep more of your intererst follow pur simple guide.

- Emergency Fund: If you are going to pay tax on your savings, use a flexible ISA, which you can use to make withdrawals during the year. (UK Gov)

- Cash ISA: Max out your £20,000 annual allowance first.

- Low-Coupon Gilts: If you have more than £20k to save and are a Higher or Additional rate taxpayer, consider moving the excess into low coupon government bonds rather than a taxed savings account.

- Premium Bonds: You can hold up to £50,000. Winnings are tax-free, making them great for those who have exhausted their Personal Savings Allowance.

- Spouse Transfer: If your partner is in a lower tax bracket, move savings into their name to use their larger (or more effective) allowances.

The Bottom Line: At 4% interest, a higher-rate taxpayer needs £12,500 (£12,500 x 4% = £500) in savings before they start paying tax. If you have more than that, it’s time to get strategic with ISAs and Gilts.

Notes

Future rule changes: savings tax rates are due to rise from 6 April 2027 to 22%, 42% and 47%, so this may get harsher next tax year.

Joint accounts: HMRC says interest on a joint account is normally split equally between the account holders unless you tell it otherwise.

A note on tax codes and self-assessment: Banks report interest directly to HMRC, so if you owe tax on savings, HMRC will usually know. If you are employed or retired and taxed through PAYE, HMRC may then collect savings tax by changing your tax code. So it is worth checking this at the start of the new tax year.